As the global beauty industry shifts toward wellness-driven solutions, nutricosmetics are emerging as a key growth area, with Shiseido leading the charge. This memorandum explores Shiseido’s quiet but influential role in shaping the nutricosmetics market, drawing on decades of expertise and its Collagen line, a hallmark of its beauty-from-within philosophy. Shiseido’s long-term commitment to nutricosmetics, often overlooked by Western markets, has allowed the company to build consumer loyalty and trust while aligning with the growing demand for holistic beauty solutions.

Rather than positioning itself with flashy new launches, Shiseido has focused on slow, consistent growth through scientific research and consumer satisfaction. The company’s strategic mastery in this space has positioned it well to capitalize on the rising global interest in nutricosmetics. As the Western beauty market acknowledges the potential of ingestible beauty supplements, Shiseido’s patient leadership provides a valuable roadmap for others looking to tap into this lucrative and growing sector.

The beauty industry is in the midst of a profound transformation, and I feel compelled to address a category that has been unjustly sidelined for far too long: nutricosmetics. For years, this category has faced skepticism. The long road we’ve walked—moving from unrecognized potential to clinically proven results—has been one of resilience and unwavering belief in the future of beauty from within.

Today, we stand at a new crossroads. While the science behind nutricosmetics is undeniable, there remain doubts within the industry about its market potential and profitability. But I challenge this outdated thinking, not with words, but with results. Year after year, TOSLA Nutricosmetics has demonstrated sustained growth, as have the brands we proudly partner with.

This memorandum is more than just a reflection on where we’ve been—it is a call to action. We offer insights and invite our peers across the industry to join us in building the future. But we cannot make this future alone. It will take the wider beauty industry’s expertise, ambition, and resources to realize the shift already underway.

The transition from topical beauty to holistic, science-backed solutions is not just an opportunity—it is inevitable. Those who recognize this will lead the industry forward. We invite you to be part of that journey as we shape the future of beauty together.

Unveiling Shiseido's Quiet Mastery in the Nutricosmetics Revolution

In a recent announcement that made waves across the beauty industry, Shiseido unveiled its new division, Shiseido Beauty Wellness (SBW), marking what has been publicized as its grand entrance into the burgeoning wellness market. The move has been described as a pivot towards holistic beauty solutions, aligning with the modern consumer’s demand for a harmonious blend of mind, body, and skincare. Yet, beneath the surface of this well-orchestrated launch lies a critical question: Is Shiseido’s latest venture indeed a new frontier for the company, or merely a strategic rebranding of a well-established legacy?

Shiseido’s foray into wellness may appear as a groundbreaking shift to the untrained eye. However, those familiar with the company’s history know that Shiseido has been a formidable player in the nutricosmetics market for decades. Their renowned product line, “The Collagen,” has been a cornerstone of their beauty-from-within philosophy, backed by almost 30 years of advanced research in collagen and skin health.

A Strategic Rebranding or Genuine Innovation?

Shiseido’s recent moves invite scrutiny. Is SBW a response to shifting market dynamics or simply a repackaging of the company’s existing capabilities under the fashionable guise of wellness? It’s crucial to consider whether this announcement represents true innovation or an exercise in strategic repositioning—an attempt to capitalize on the global interest in holistic beauty.

Shiseido’s deep roots in the nutricosmetics industry give them a significant advantage. As one of the early entrants into this niche, they have built trust and loyalty among consumers, particularly in Japan, where their nutricosmetics have enjoyed more visibility. Despite this, Shiseido’s reputation as a skincare and cosmetics giant often overshadows its contributions to the nutricosmetics field, leading to a perception that they are newcomers to this space.

The truth, however, is far more complex. Shiseido has been playing a long game that has often gone unnoticed by Western markets. Their quiet dominance in the nutricosmetics sector is a testament to their strategic foresight and patience—starkly contrasting the flashy, short-term tactics many of their competitors favored.

The Subtle, Calculated Play of a Market Leader

Shiseido has charted a different course in the high-stakes beauty industry, where immediate results and eye-catching products often steal the spotlight. Their approach has been one of quiet persistence, allowing their products and the loyalty of their customers to speak volumes. “The Collagen,” their flagship nutricosmetic product, exemplifies this strategy. It has been fortifying skin health from within for decades, supported by relentless research and development. This move seems almost prophetic as the global market matches the wellness trend.

To many in the Western beauty industry, nutricosmetics have long been dismissed as a niche market, a mere footnote in the broader landscape of beauty and skincare. Shiseido, however, recognized the potential of this category early on. They understood that true beauty extends beyond surface-level treatments and requires a deeper, more holistic approach. While the concept of “collagen banking” has traditionally focused on topical treatments—like collagen-based serums, sun protection, LED light therapy, and chemical peels—Shiseido saw the value in complementing these with ingestible beauty. Long before supplements became a popular part of the conversation, they recognized that nourishing the skin from within could be key to delaying the signs of aging.

While others in the industry were focused on quick fixes and instant gratification, Shiseido played the long game, akin to a master chess player who anticipates moves far ahead of the competition. Their nutricosmetics didn’t need flashy marketing or grandiose claims; the results and their consumers’ quiet, enduring loyalty were proof enough.

A Revolution Years in the Making

What Shiseido’s executives grasped, and what many of their Western counterparts failed to appreciate, is that beauty is not just skin deep. It is intrinsically linked to long-term well-being, and the benefits of this approach are only now becoming apparent to a broader audience. As the Western market belatedly awakens to the value of nutricosmetics, Shiseido finds itself in a position of strength, having laid down roots in this sector that are nearly impossible to dislodge.

Today, as the Western beauty industry finally begins to acknowledge the importance of beauty from within, Shiseido stands at the forefront not as a newcomer, but as a seasoned leader who has been quietly shaping the market from behind the scenes. In a world where the loudest voices often dominate, Shiseido’s story is a powerful reminder that true innovation sometimes happens in the shadows, far from the spotlight.

Ultimately, the unveiling of SBW may not be the start of a new journey but rather the culmination of decades of strategic planning and relentless innovation. As the rest of the world scrambles to catch up, Shiseido’s position is clear: they’ve been leading the wellness revolution all along.

The Nutricosmetics Market: A Landscape of Opportunity and Scrutiny

In recent years, the global nutricosmetics industry has witnessed a surge in both popularity and innovation. More than 600 brands now populate the Nutricosmetics 2030 map, each vying for dominance in a rapidly expanding market that fuses nutrition and beauty. At its core, the industry taps into a growing consumer desire to enhance appearance and wellness from within, offering products that promise to improve skin, hair, and overall health. While this burgeoning sector holds immense promise, it also faces growing concerns regarding product quality, transparency, and the scientific validity of its claims.

A Rapidly Expanding Market

Nutricosmetics—dietary supplements designed to promote beauty from the inside out—ride a wave of consumer interest. The appeal is clear: consumers increasingly seek ingestible products that promise holistic beauty benefits rather than relying solely on topical treatments. By 2030, the global nutricosmetics market is projected to reach unprecedented heights, with industry titans and nimble startups competing for a piece of the pie.

Beauty industry leaders such as Shiseido, known for their dominance in traditional skincare products, have expanded their offerings by entering the market for ingestible beauty supplements. These established companies view nutricosmetics as a natural extension of their product lines, in line with the growing trend towards overall wellness and holistic health. Meanwhile, newer companies entering the market are using creative formulations and marketing approaches to appeal to younger, health-conscious consumers who prioritize transparency and effectiveness.

The Rise of Powders and Liquids

A clear shift is emerging in product formats. While capsules have long been the staple of dietary supplements, nutricosmetics are increasingly offered in powder and liquid forms. These formats, including collagen powders and hyaluronic acid drinks, are gaining popularity due to their perceived ease of use and potency. Consumers can seamlessly integrate these products into their daily routines, adding a scoop of powder to their morning smoothie or sipping a beauty elixir throughout the day.

But why the shift away from capsules? Experts believe consumer preferences are shifting towards products that offer convenience and simplicity. Capsules are criticized for taking a long time to show results due to having lower potency, which may lead people to take multiple capsules at once, making it unsustainable. This creates a competitive advantage for brands that can match consumer expectations.

The True Test of Nutricosmetic Efficacy

Despite the hype surrounding new product formats, the industry faces a deeper, more complex issue: ingredient effectiveness. The value of nutricosmetics hinges on the bioavailability and quality of the active ingredients, but not all brands meet the same standards in this regard. Consumers, becoming increasingly informed, ask more complex questions about what they’re putting into their bodies. Does the collagen in their beauty supplement improve skin elasticity? Are the antioxidants in their hair supplement potent enough to make a difference?

Some brands invest heavily in clinical trials and research to validate the efficacy of their products. Yet, others rely on savvy marketing strategies to sell products based more on trends than science. While collagen, vitamins, and antioxidants are touted as essential ingredients in many nutricosmetics, the challenge for manufacturers lies in delivering these ingredients in a form that the body can effectively absorb. Emerging technologies such as advanced encapsulation techniques and enhanced nutrient delivery systems promise to improve this, but these advancements are still not widely adopted across the industry.

Moreover, the lack of enforcement of ingredient potency and efficacy regulations remains a critical issue. With no universally accepted benchmarks, consumers are left to navigate a landscape that can be confusing at best and misleading at worst. For the industry to sustain its growth and credibility, these gaps in regulation must be addressed.

A Competitive Landscape

The competition within the nutricosmetics sector is fierce, with established conglomerates such as L’Oréal, Nestlé, and Shiseido competing against a new wave of disruptors. While larger companies benefit from robust research and development capabilities, smaller brands are gaining traction by appealing to niche markets. Vegan ingredients, personalized beauty solutions, and eco-friendly formulations are among the trends driving growth for smaller players.

The question remains: how long can these startups remain independent? The current trend of market fragmentation could give way to consolidation as industry giants seek to acquire innovative startups to expand their nutricosmetics portfolios. Strategic acquisitions will likely accelerate as the sector becomes more lucrative, reshaping the competitive landscape.

The Regulatory Challenge

As we move towards 2030, the nutricosmetics market is experiencing significant growth. However, there remains a critical unresolved issue: the absence of stringent regulatory oversight. Unlike pharmaceuticals, nutricosmetics exist in a regulatory grey area where marketing claims often outpace scientific validation. Regulations differ significantly across regions, with some countries demanding more substantial evidence of efficacy than others. This inconsistency presents both challenges and opportunities for brands aiming to establish credibility and transparency.

In both the EU and the U.S., nutricosmetics—classified as food supplements in the EU and dietary supplements in the U.S.—do not require pre-market authorization. Instead, manufacturers can introduce these products without prior approval, relying on post-market surveillance to ensure safety and regulatory compliance. This regulatory structure places the responsibility on manufacturers to ensure product safety and accurate labeling, while regulatory agencies monitor these products once they’re on the market to address any safety concerns.

To succeed long-term, brands must focus on innovation and accountability. Those who invest in clinical research, transparent labelling, and consumer education will likely emerge as leaders in this expanding market. However, brands exploiting regulatory gaps could face significant backlash as both consumers and regulatory bodies grow more discerning and stricter oversight is introduced.

The Path Towards 2030

The nutricosmetics industry stands at a crossroads. On the one hand, it offers numerous opportunities for innovation and growth. On the other, it faces scrutiny over transparency, efficacy, and regulation issues. As the sector matures, it will need to navigate these complexities to meet the evolving demands of consumers who are no longer satisfied with vague promises and superficial benefits.

The future of nutricosmetics lies in delivering on its core promise: beauty from within. But achieving this will require more than clever branding. It will demand a commitment to scientific rigor, regulatory alignment, and consumer trust. As the industry approaches 2030, the question remains—who will rise to the challenge, and who will fall short?

The Nutricosmetics Market Size Dilemma: Uncovering the Truth Behind the Numbers

A recent analysis of the UK nutricosmetics market, which our company commissioned and conducted at significant expense, has sparked a debate within our organization. The report claimed that the total value of the entire sector is $26.81 million with a compound annual growth rate (CAGR) of 6.65% across 46 brands, and more brands are still being added. This value was only slightly more than the combined revenues of the two UK brands for which we have reliable data. This significant difference raises important questions: Why is the nutricosmetics market undervalued, and why hasn’t anyone in the industry challenged these figures?

A Tale of Two Approaches

The valuation issue highlights two fundamentally different approaches to nutricosmetics. In Japan, the market is vibrant and dominated by beauty brands that market these products as fun, fresh, and rejuvenating. In contrast, in the Western markets—particularly the EU and USA—nutricosmetics are primarily promoted by health and food companies. These regions often focus on aging, pain relief, and lost beauty, creating a stark difference in consumer perception. While Japan celebrates aging positively, the West views it more negatively.

Analyzing the Market

To better understand the global nutricosmetics market, we analyzed data from several years and the most recent publicly available information. Japan’s mature market was used as a benchmark due to its higher proportion of working-age and elderly populations, which makes it an ideal comparison point.

We also examined the Slovenian market, a micro EU member state, which we consider well-developed. For a broader context, we modeled the EU and USA markets using critical demographic and economic indicators: population size, the proportion of active and elderly populations, and GDP per capita. For Japan and Slovenia, we had reliable data on the size of the nutricosmetics market, enabling us to estimate figures for the less mature EU and USA markets.

Market Penetration Disparities

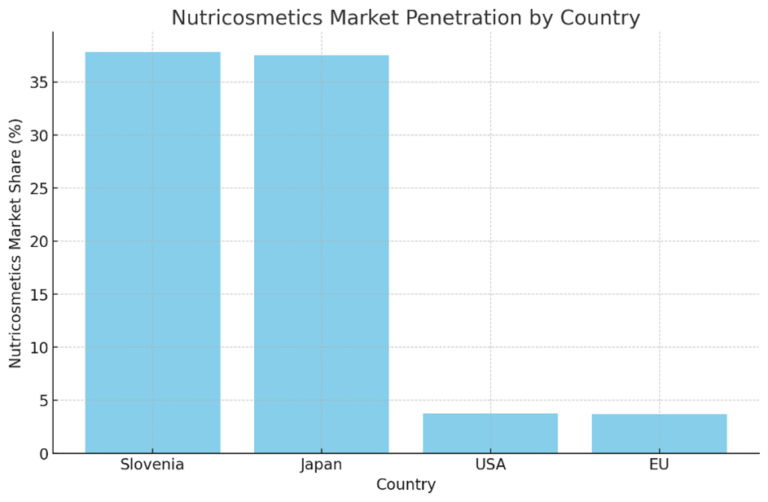

Our analysis revealed a significant gap in nutricosmetics market penetration between the Japanese and Western markets. In Japan, nutricosmetics account for approximately 37.5% of the total supplement market. In contrast, the USA and EU have a much lower penetration rate of around 3.7%. This stark difference highlights a substantial growth opportunity in the Western markets if they can achieve market dynamics similar to Japan’s.

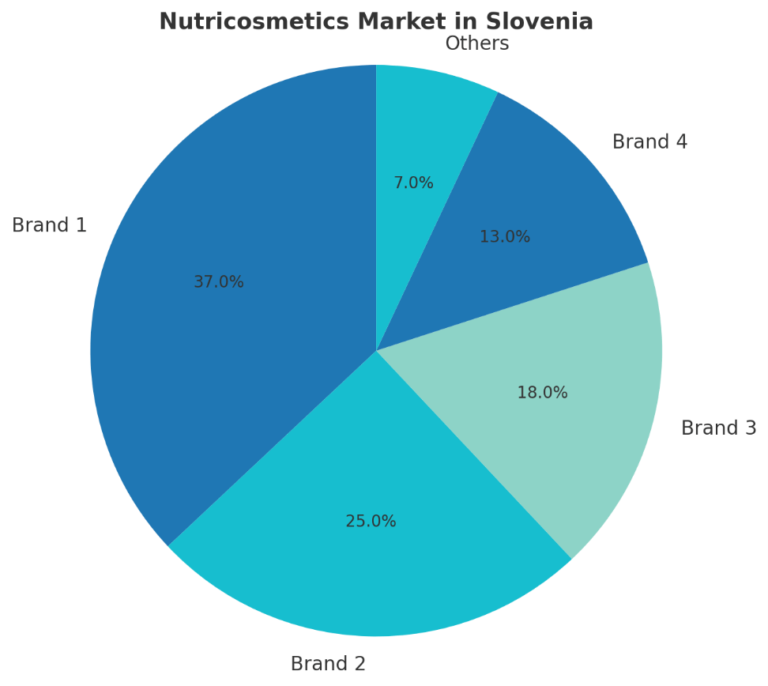

I mentioned earlier that we selected Slovenia as a developed market comparable to Japan. The data shows that Slovenia is at the forefront, with a 37.81% penetration of nutricosmetics products in total food supplement sales in the country. The data was obtained from national import sources, retail and pharmacy association data, and from the major distribution companies that directly collaborate with the largest retailers in the country. I cannot guarantee the absolute accuracy of the information provided, but it is reasonably reliable.

Per Capita Spending on Nutricosmetics

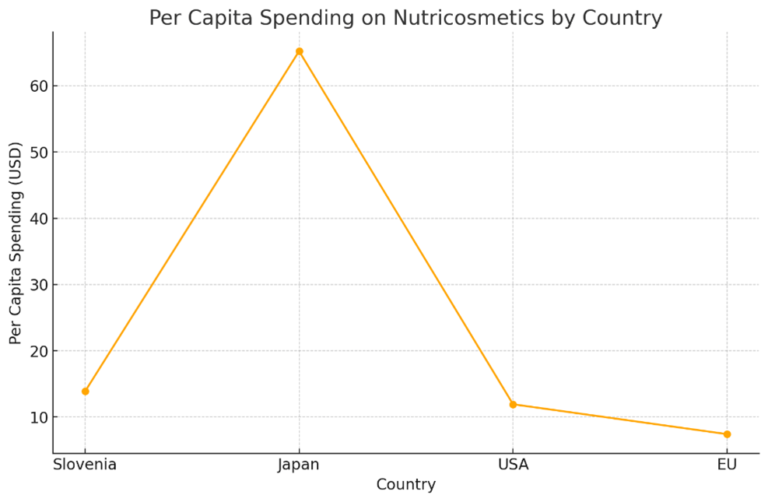

Further, the analysis showed that per capita spending on nutricosmetics is substantially higher in Japan compared to Slovenia, the USA, or the EU. This difference in consumer behavior underscores Japan’s market maturity and the potential for increased spending in Western markets if they can shift consumer perception and marketing strategies.

When it comes to the per capita consumption of nutricosmetics, Slovenia stands on par with the United States. At first glance, both countries appear to have similar spending levels—$14 per person in Slovenia mirrors the U.S. But when factoring in GDP per capita, the landscape shifts dramatically. Slovenia’s GDP per capita is just 41.3% of the U.S.’s, meaning that the $14 spent by Slovenes is equivalent to $29 per capita in the United States when adjusted for economic output. This adjustment paints a striking picture: Slovenians consume nutricosmetics at a rate 142% higher than many market research reports suggest for the U.S.

Yet, this demand is still far behind what we see in leading markets like Japan, where nutricosmetics have a more entrenched consumer base. Similar calculations applied to the European Union show an even greater upside: a 235% increase, equating to $25 per capita. These numbers imply that the U.S. and EU markets are undervalued by $2.85 billion and $9.6 billion, respectively—figures that underscore the untapped potential in these regions.

In the following analysis, I will break down how these numbers were derived and what they reveal about the global nutricosmetics market.

Potential Market Size Projections

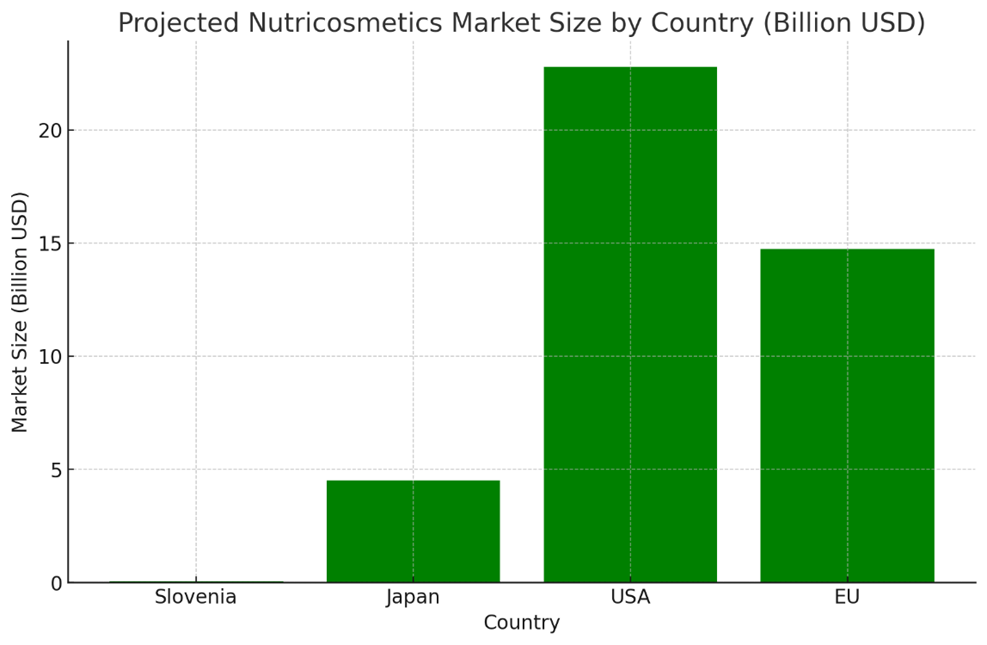

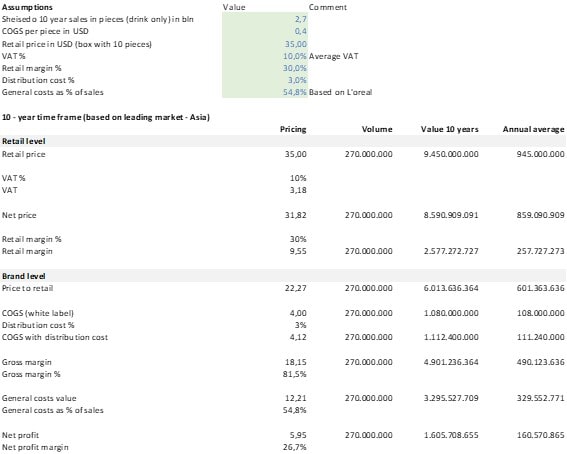

If the USA and EU markets were to reach penetration levels similar to those of Japan, the nutricosmetics market could be valued significantly higher. The projected figures suggest that the USA market could grow to $23 billion, and the EU could reach up to $15 billion in the next two to three decades. These projections are based on modeling the projected market sizes using supplement sales data from Japan and Slovenia.

These figures point to a strong likelihood that by 2040, the age structure of the population in the U.S. and EU will closely mirror that of Japan, following similar demographic trends. With aging populations and the strain on pension systems—especially in Europe—people will be compelled to stay active longer. Alongside that, there will be a growing desire to maintain a youthful appearance well beyond today’s retirement age.

When we factor in these demographic shifts, combined with GDP growth projections for both regions, and compare them to current nutricosmetics consumption levels in Japan and the overall industry’s state of mind, the conclusion becomes clear: the potential for market expansion in the U.S. and EU is significant, echoing the conclusions of my analysis.

The Role of Perception and Positioning

A key reason for this undervaluation is how beauty supplements are priced and perceived. Despite being similar in composition to other food supplements, beauty supplements command higher prices because they are associated with cosmetic benefits. However, many supplements in the EU and USA are marketed as general food supplements, missing the opportunity to be recognized—and priced—as nutricosmetics. This misclassification results in a significant loss of market value.

INTERESTING: The provided link leads to an Indonesia-based user-generated blog post about collagen. The product is prominently placed in the heart of the department store and is being promoted just like any other premium beauty-cosmetics product.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Above is a collage of photos showcasing nutricosmetics brand placements taken in September 2024 at high-end department stores in Slovenia and the Philippines. Interestingly, these products are positioned right next to major beauty brands, a sight you won’t often see in most parts of the Western world.

In Japan, marketers have successfully positioned these products in the beauty industry, sparking consumer interest and market growth. However, in the West, the market is mainly dominated by food and health companies. These companies find it challenging to sell premium products and do not fully tap into the potential of beauty supplements. I refer to this as the catalyst effect.

The Impact of Supply Chains and Consumer Loyalty

The origin and quality of products are key factors contributing to the nutricosmetics market’s undervaluation. Many supplements in the U.S. are imported from China and India, where they often fail to meet the three critical criteria for successful nutricosmetics: simplicity, palatability, and validation. These pillars are not just crucial for establishing trust, but also for driving repeat purchases and building long-term consumer loyalty and value. When a product misses one or more of these pillars, it is frequently relegated to the lower-priced food supplement category, rather than being positioned as a premium beauty product.

Frankly, the moment consumers become aware of the product’s quality and origin, it directly impacts the sales proposition offered to them. And while I hope this observation doesn’t offend anyone who may recognize their own practices here, the fact remains: this approach may appeal to cost-conscious consumers in the short term, but it doesn’t foster the same level of engagement and loyalty as nutricosmetics that fully deliver on these three pillars.

As a result, a significant opportunity is being missed. If these products were better aligned with the expectations and standards of the nutricosmetics market, they could command higher prices and foster a loyal customer base that values quality and efficacy over cost alone.

Connecting this to broader market dynamics, the undervaluation and misclassification of these products in the U.S. and EU highlight a critical gap. While Japan’s nutricosmetics market thrives due to its alignment with consumer expectations, Western markets lag behind, missing out on substantial growth opportunities. The shift from general food supplements to targeted, ingestible beauty products—driven by the increasing demand from an aging population—represents a major growth area. However, realizing this potential requires a strategic pivot towards ensuring that nutricosmetics meet the high standards necessary to build consumer trust and loyalty.

By addressing these gaps, the nutricosmetics market in the U.S. and EU could grow exponentially, achieving the same level of market penetration and consumer engagement seen in Japan.

Implications for the Industry

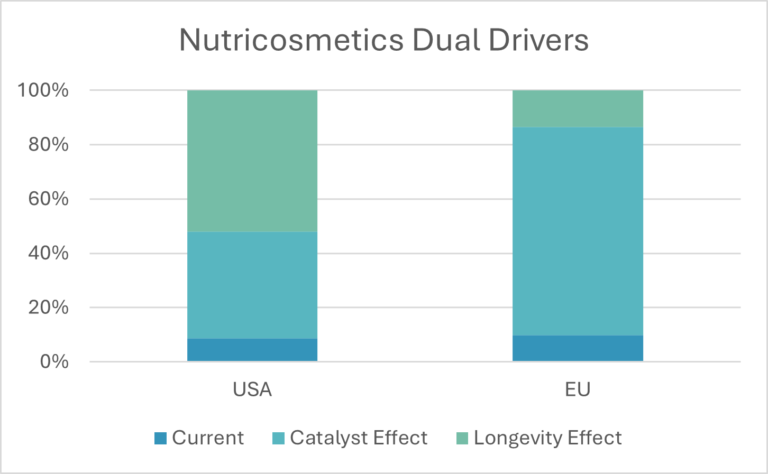

The nutricosmetics market in the West is significantly undervalued, primarily due to misclassification and poor market positioning. Currently, these regions exhibit much lower market penetration than Japan, which can be attributed to differences in how these products are marketed and perceived. The data suggests that if these markets adopt a similar approach to Japan, where beauty brands drive the nutricosmetics sector, the market could grow exponentially. By 2040-2050, the US market alone could be worth up to three times the generally accepted size of the nutricosmetics market, which is currently capped at about 8 billion USD. The EU market could reach almost twice this value, indicating a significant shift in marketing strategy and consumer perception. This implies for both markets a compound annual growth rate (CAGR) of between 11-15 percent, significantly higher compared to publicly available estimates.

The graph below illustrates the contrasting dynamics between the USA and EU nutricosmetics markets, highlighting each region’s distinct opportunities. In the EU, marked by its aging population, there is a significant opportunity to leverage the “Catalyst Effect.” This suggests that the market could grow substantially if beauty companies effectively target and market nutricosmetics to older consumers.

On the other hand, the “Longevity Effect” is projected to have a less pronounced impact in the EU compared to the USA. The relatively younger population in the USA is expected to drive the market to new heights in the coming decades. The “Longevity Effect” will play a crucial role in the USA, where the growing interest in wellness and preventative care among a younger demographic will significantly boost demand for nutricosmetics, making it a key driver of market expansion.

This comparison highlights the need for tailored strategies in each market. EU brands should maximize the “Catalyst Effect,” while the USA should capitalize on the emerging “Longevity Effect.”

Realizing this potential will require a shift in how these products are marketed and sold—away from the health and food sectors and into the hands of beauty brands that understand the value proposition. The question is whether the industry will seize this opportunity or continue to leave billions of dollars on the table.

Shiseido: The Silent Dominator in Nutricosmetics and the Global Beauty Industry’s Missed Opportunity

The nutricosmetics market has become one of the most intriguing and competitive battlegrounds. Beauty companies worldwide are grappling with how to incorporate ingestible supplements into their portfolios—products that promise beauty from within, enhancing skin, hair, and overall health. But while many significant players in the USA and EU continue to struggle with pills and powders, Shiseido, the Japanese beauty giant, has quietly become a leader in this space with an alternative form.

In 2002, L’Oréal, in partnership with Nestlé, launched Innéov, a pioneering nutricosmetic brand. Innéov was presented as a series of potent nutritional supplements tailored to address beauty concerns, including enhancing hair strength and volume, preparing skin for sun exposure, and providing anti-aging skincare benefits. Despite its innovative approach, Innéov faced significant challenges; L’Oreal and Nestle ended the venture in 2014:

- Market acceptance: The product was perceived as too technical and lacked emotional appeal, which is crucial in the beauty industry.

- Regulatory hurdles: Innéov struggled with stringent health claim regulations, especially in the EU. The EU’s strict policies on health claims limited Innéov’s ability to market its benefits effectively.

- In a renewed effort, this January, L’Oréal, together with Nestlé and several VCs, invested CHF 56mn in Series D of a Swiss biotech health, aging and longevity company called Timeline. The investment interest centred on Timeline’s proprietary technology, Mitopure, a product based on Urolithin A. In this case packaging and marketing of the brand are more aligned with current beauty trends; however, it still leans towards a pharmaceutical appearance (pill) rather than a beauty-centric one and may face similar challenges.

- Regulatory and ingredient challenges: Urolithin A, being technical, faces similar challenges in claim substantiation as Innéov did for its ingredients. While scientifically robust, translating its benefits into consumer-friendly and regulator-approved claims remains complex. It is not possible to explain the benefits of Mitopure/Urolithin A without interfering with health claims, which are not allowed.

- L’Oréal’s experience in the nutricosmetic sector highlights the importance of emotional appeal, consumer understanding, regulatory navigation, and market-friendly product presentation. Future success in this sector depends on harmonizing scientific innovation with consumer expectations and regulatory compliance.

TOSLA’s insider view: “Nutricosmetics has evolved into a category that major players in the beauty industry can no longer afford to overlook. The recent investment in Timeline underscores this trend, yet it also highlights a recurring challenge: regulatory hurdles. Collagen-based products emerge as a promising solution, as they navigate regulatory constraints more smoothly, making them ideal for driving industry growth. Moreover, the widespread use of collagen in beauty skincare products enhances market adoption and fosters consumer awareness of this key ingredient. However, while the entry of big players might prompt hopes for regulatory changes, such shifts are unlikely, as they could potentially clash with interests in the pharmaceutical sector.”

Shiseido’s story is particularly compelling because the company has flown under the radar for so long. Despite being an early innovator in nutricosmetics, Shiseido only recently revealed its global ambitions, catching Western beauty brands off guard. Shiseido’s success highlights the differences in how various markets—like Japan, Slovenia, the EU as a common market, and the USA—have developed and consolidated and why the Western beauty industry may have underestimated this sleeping giant.

Market Development: Slovenia and Japan Lead the Way

Slovenia and Japan present distinct yet complementary cases when it comes to nutricosmetics market development. While Slovenia is a smaller market, it is highly consolidated, with a few dominant players controlling most of the share. The rapidly aging population drives strong demand for anti-aging and wellness products, including nutricosmetics. However, Slovenia’s global impact remains modest due to its smaller scale and market influence.

In contrast, Japan has emerged as a pioneering force in the nutricosmetics space. Shiseido, a trailblazer in the beauty-from-within category, introduced its iconic The Collagen line in 1996 and has since built lasting consumer trust. With Japan’s aging population and a cultural emphasis on holistic wellness, the market was primed for nutricosmetics, particularly in liquid form. Liquids have gained significant traction in Japan as consumers prioritize convenience, simplicity, and perceived effectiveness. Liquid nutricosmetics are viewed as more natural and easier to incorporate into daily routines compared to pills or powders. Shiseido’s domestic success laid the foundation for its international expansion, significantly influencing the global nutricosmetics landscape.

Slovenia’s embrace of larger-format liquid nutricosmetics, ranging from 300ml to 700ml bottles, offers a valuable blueprint for the future development of beauty supplements in Western markets. Slovenian consumers’ preference for practicality and prolonged use, combined with an emphasis on elegant, minimalist packaging, highlights the aesthetic appeal of these products. This suggests that in the West, nutricosmetics should be positioned not only as supplements but also as premium lifestyle products. By merging functionality with sophistication, liquid nutricosmetics can seamlessly integrate into daily routines, catering to the growing demand for beauty from within.

USA and EU: Fragmented and Unprepared

In contrast, the nutricosmetics markets in the USA and EU are highly fragmented, with numerous small and medium-sized players competing for consumer attention. In the USA, the trend is still emerging, driven primarily by direct-to-consumer brands and wellness startups that leverage social media and e-commerce platforms to build their presence. However, these brands face intense competition, and their reliance on capsule, pill, and powder formats, often seen as less enjoyable and less effective by consumers, hampers their growth potential. This format preference creates a barrier to deeper consumer engagement, limiting their ability to capitalize on the growing interest in beauty-from-within solutions fully.

The EU market presents significant complexities, particularly for brands looking to scale across the region. While countries like France and Germany show strong consumer interest in beauty supplements, the regulatory landscape is fragmented, creating challenges for companies trying to achieve consistent growth. One of the main hurdles is the strict regulations around health claims, which can severely limit how brands are allowed to promote their products.

Many companies attempt to push for health claims, but they would be better served by focusing on beauty claims instead. Sticking to well-known ingredients like collagen, hyaluronic acid, or biotin simplifies the messaging, as these ingredients already have strong consumer recognition. There’s little need to over-explain their benefits, allowing brands to avoid the stringent requirements associated with health-related claims. This approach not only streamlines compliance but also enables more effective marketing strategies.

By concentrating on beauty outcomes rather than health promises, brands can navigate the regulatory environment more efficiently. This has been a key factor in the success of companies like Shiseido, which has focused on beauty claims to penetrate the European market. Their agility in avoiding the regulatory bottlenecks has allowed them to expand relatively uncontested, highlighting the advantage of a beauty-first strategy in a complex regulatory market like the EU.

The Secret Villain: Shiseido’s Global Strategy Unveiled

Here’s where Shiseido plays the role of the silent disruptor. For years, the company operated its nutricosmetics business almost exclusively in Asia, quietly observing the trends and refining its products. While Western beauty brands were still catching up, Shiseido had already amassed significant expertise and market share with its liquid collagen products. Shiseido has revealed its long-term strategy as the USA and EU markets finally begin to show promise for nutricosmetics.

Shiseido’s move is significant because it was already present in the USA and EU markets through its traditional beauty brands. Still, it kept its nutricosmetics division relatively hidden. This allowed the company to bide its time, testing its products in more favorable markets (such as Japan and other parts of Asia) before moving into the West.

Now, Shiseido is strategically poised to leverage its brand equity in traditional beauty products to introduce its nutricosmetics line on a global scale. Its recent investments in The Collagen and other liquid products signal a more aggressive push into North America and Europe, surprising many Western beauty brands. With decades of experience and a consumer base already familiar with its products, Shiseido can quickly scale in markets where other brands are still experimenting. Although this may seem like a bold statement, there are indications that the SBW could already be generating tens of millions of dollars in those two markets.

Collagen: The Trojan Horse of Nutricosmetics

A crucial part of Shiseido’s success lies in its strategic use of collagen as a foundational product. Collagen is a well-known ingredient with established beauty benefits, such as supporting skin elasticity and hydration and reducing signs of aging. Unlike more complex, lesser-known ingredients, collagen doesn’t require a deep educational push to explain its value to consumers. This makes it an ideal entry point for brands looking to build a presence in the nutricosmetics market.

Collagen products are more accessible to market and more palatable to consumers and regulators alike. Shiseido’s decision to focus on collagen has allowed it to side-step many of the challenges other brands face when introducing more obscure ingredients. By leading with a product that is already trusted and understood, Shiseido can then expand its product offerings to include more specialized or technical nutricosmetics once the brand is firmly established in new markets.

A New Era of Consolidation?

As Shiseido ramps up its global expansion, the nutricosmetics market is likely to undergo consolidation. In fragmented markets like the USA and EU, where smaller players have made early inroads but struggle to scale, more giant beauty conglomerates will likely seek partnerships and acquisitions to bolster their nutricosmetics offerings. With its established dominance in Asia and strong footing in liquid products, Shiseido is well-positioned to lead this charge.

Understanding consumer preferences will be the key for any company looking to compete in this space. As Shiseido has shown, format matters. Liquid products, which are convenient, enjoyable, and perceived as more effective, are the future of nutricosmetics. Brands that fail to adapt to this reality may be outpaced by competitors already mastering the game.

Final Thoughts

Shiseido’s rise in the nutricosmetics space is a lesson in market timing and a reminder of how under-the-radar strategies can catch entire industries by surprise. While the USA and EU beauty markets have been slow to embrace nutricosmetics, focusing on pills and powders, Shiseido has quietly built a formidable presence, using its liquid collagen products as a Trojan horse to enter new markets.

As beauty consumers in the West become more educated about beauty-from-within solutions, Shiseido is poised to reap the rewards of its long-term strategy.

A noteworthy aspect of Shiseido's nutricosmetics strategy is the relatively low investment in aggressive growth initiatives. Instead, it appears the division has been treated more as a supplementary “drag-along” program, rather than a standalone growth engine. When modeling this dynamic, particularly using competitor data such as L’Oréal’s, it made sense to assign a more favorable cost structure to the division's overall contribution, as it has not absorbed the same level of expansion-related expenses.

While exact profitability figures remain under wraps, industry insiders suggest that the nutricosmetics division plays a critical role in bolstering Shiseido's bottom line, potentially balancing out weaker performances in its other beauty sectors. As Shiseido sets its sights on Western markets, it aims to replicate the success it has enjoyed in Japan and Asia, with nutricosmetics positioned as a key driver in its broader global strategy.

The Untapped Potential of Nutricosmetics

In the beauty world, skincare giants have long dominated the narrative, pushing products that promise glowing, youthful skin. But beneath the glossy surface of creams, serums, and moisturizers lies an overlooked segment quietly gaining traction: nutricosmetics. While beauty insiders often dismiss these supplements as a passing trend, the numbers tell a different story—substantial profitability and unmatched customer loyalty. Could nutricosmetics, particularly those in liquid form, represent the next frontier for an industry long reliant on superficial solutions?

A Closer Look at the Numbers

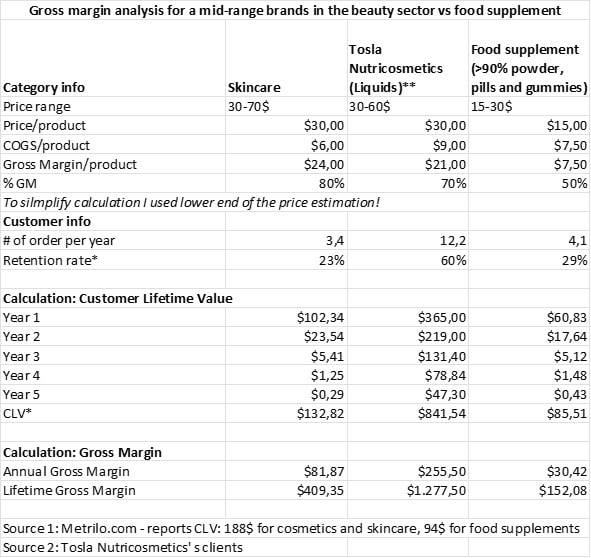

The beauty industry, worth over $500 billion globally, has remained primarily anchored to topicals, where the fight for market share is as fierce as it is expensive. Skincare products, typically priced between $30 and $70, offer decent margins, but high customer acquisition costs and low purchase frequency often plague them. Most consumers replenish their skincare products only three to four times a year, leading to lower customer lifetime value (CLV) and a constant need for brands to reinvent their marketing strategies to maintain loyalty.

In contrast, nutricosmetics—products that enhance beauty from within, typically through vitamins, minerals, and antioxidants—present a radically different business model. These supplements, mainly when produced in liquid form, can be priced similarly to skincare products but benefit from a much higher retention rate. Combining insights from our clients and discussions with partner brands, we discovered that consumers buy nutricosmetics an average of 12 times annually, with more than 60% returning for repeat purchases. The result? A CLV of over $800 per customer is more than triple the lifetime gross value of a traditional skincare consumer.

The repeat-buy nature of nutricosmetics, coupled with a retention rate of 60%, is a statistic that any beauty executive would envy. But why, then, are so many beauty experts hesitant to embrace this emerging category? The answer lies in a misunderstanding of what drives profitability in the long run.

The Real Profits Lie in Retention

The skepticism surrounding nutricosmetics is primarily based on the assumption that these products function like other food supplements—low cost, low margin, and ultimately, low value. But this assumption overlooks a crucial fact: nutricosmetics is not a one-time purchase game. It’s a marathon, not a sprint. Unlike skincare, where a customer might purchase a high-end cream once every three months, nutricosmetics foster a more frequent engagement.

A beauty brand selling a $30 skincare product with a gross margin of 80% can expect a healthy return—assuming that customers return for more. However, most skincare products require continuous advertising to keep customers loyal. Consumers quickly jump to the next best thing when a brand’s marketing falters, eroding profitability.

Nutricosmetics, however, are driven by habit. Customers who experience tangible results, such as improved skin elasticity, hair growth, or a clearer complexion, become loyal to the product and the regimen. The analysis shows that a $30 nutricosmetic liquid product, with a gross margin of 70%, benefits from more consistent purchasing behaviour. Consumers who buy these products once are highly likely to buy them repeatedly. Over time, the gross lifetime value of these customers far surpasses those in the skincare category, not because the margins are drastically higher, but because the products build a kind of brand loyalty that skincare can’t match.

The Power of Liquid Format

At the core of customer loyalty is a critical factor: format. In the competitive nutricosmetics space, the right format can define a product’s success. TOSLA, a leader in liquid supplements, has built its model on three essential pillars that validate the liquid format: validation, simplicity, and palatability. The liquid format is scientifically validated for effectiveness, offers simplicity in daily use compared to complex pill regimens, and is far more palatable than powders or capsules. These factors resonate with consumers, leading to higher satisfaction and long-term loyalty to the product.

The liquid format also provides greater versatility in formulation, allowing for higher concentrations of active ingredients. Thanks to TOSLA’s proprietary masking technologies, even potent ingredients can be delivered in a palatable way, making the liquid format more consumer-friendly. This technological edge enhances the product’s overall appeal and effectiveness and supports its premium positioning, aligning it with the value perception of skincare products.

An Overlooked Revenue Stream

For beauty brands and direct-to-consumer companies seeking new growth avenues, nutricosmetics offer a largely untapped revenue stream, poised to ease the strain of an increasingly crowded skincare market. Despite pouring millions into skincare innovation, the opportunity cost of ignoring this burgeoning sector is becoming more difficult to justify.

Take, for instance, a typical beauty brand that sells skincare products priced at $30 with an 80% gross margin, generating an average customer lifetime gross value of roughly $250—assuming a retention rate of 23%. Now, envision that same company launching a nutricosmetics line, similarly priced at $30, but benefiting from the unique purchase patterns of beauty supplements. Nutricosmetics, if formulated effectively, encourage daily use, driven by their palatability, pleasurable texture, and appealing scent. Users expect noticeable results within three months, but only if they take the product consistently. This necessity for regular consumption pushes customers to reorder, with an assumed retention rate of 60%, resulting in 12 purchases per year for a monthly supply.

The math is simple: without raising prices, the lifetime value of a customer in the nutricosmetics category skyrockets to $800, purely from the repeat-purchase behavior that the supplements incentivize. For beauty brands navigating a competitive landscape, it’s an opportunity too valuable to overlook.

Why the Beauty Industry Should Take Notice

Despite the clear advantages, the beauty industry has slowly embraced nutricosmetics, particularly in liquid form. Some industry insiders remain skeptical, citing concerns over regulation and efficacy claims. Others fear that expanding into nutricosmetics would dilute their brand’s core identity. But these concerns are shortsighted.

In an age where consumers are increasingly looking for holistic solutions that blend beauty with wellness, nutricosmetics are perfectly positioned at the intersection of these trends. The rise of ‘beauty from within’ is not just a fad—it’s the industry’s future. Beauty companies that fail to recognize this shift risk being left behind, while those that do will reap the rewards of higher margins, more excellent customer retention, and, most importantly, a much larger lifetime value.

Nutricosmetics is far from just a buzzword—it is a new business model, one that challenges the way we think about beauty, customer loyalty, and long-term profitability. For companies willing to embrace this shift, the rewards are clear. The only question left is: Will the beauty industry listen?

Conclusion

As the global beauty industry undergoes a seismic shift, the role of nutricosmetics in redefining beauty from within is becoming undeniable. Shiseido’s quiet yet calculated approach to this revolution is a testament to the company’s foresight and deep understanding of beauty and wellness trends. While Western markets have been slow to embrace the holistic benefits of ingestible beauty supplements, Shiseido has been patiently nurturing this category for decades, particularly with its flagship product, The Collagen.

With consumers increasingly seeking long-term solutions beyond the surface, nutricosmetics offer brands an untapped revenue stream characterized by higher retention rates and customer loyalty. Shiseido’s mastery of the liquid format, backed by scientific validation and consumer-friendly formulations, has positioned it not as a newcomer but as a pioneer in this space. As the West catches up to the beauty-from-within trend, Shiseido’s leadership and long-standing commitment to nutricosmetics place it in a unique position to shape the industry’s future.

The beauty landscape is evolving, and Shiseido has already proven that the quietest players can often lead the most profound revolutions. The question is whether the rest of the beauty world is ready to follow suit or risk being left behind in this new era of holistic beauty.

Legal Information and Disclosures

This memorandum reflects the views and opinions of the author as of the date indicated and is provided for informational purposes only. The content may be subject to change without notice, and there is no obligation to update the information herein. Tosla Nutricosmetics makes no representation or warranty regarding the accuracy or completeness of the information contained in this memorandum.

This document is not intended as an offer or solicitation to buy or sell any products or services, nor should it be interpreted as providing professional advice of any kind. Any forward-looking statements or industry trends mentioned in this memorandum are based on publicly available information and third-party sources deemed to be reliable; however, Tosla Nutricosmetics does not guarantee the accuracy or completeness of such information and has not independently verified it.

The reader is cautioned that past performance or trends in the nutricosmetics or beauty industry do not necessarily predict future outcomes, and any projections of future performance are inherently uncertain. Investments in business ventures or products related to this field may involve risks, and there is no assurance of profitability or success.

This memorandum, or any portion thereof, may not be reproduced, distributed, or transmitted in any form without prior written consent from Tosla Nutricosmetics.